AMP is attempting one of the most complicated turnarounds in corporate history (if not a gold medal winner). Brett Le Mesurier (Senior Analyst – Shaw and Partners) says “I can’t recall another company which is fighting its distribution, has declining revenue margins, increasing net outflows, implementing a substantial expense reduction program and facing potentially large remediation and litigation costs all at the same time.” The question for investors is whether AMP is cheap enough at current prices to warrant being part of a portfolio when all these issues are considered.

Matt Williams (Portfolio Manager – Airlie Funds Management) however believes that if the company were to be broken up, the sum of parts could be worth more than $2.20 per share, but stresses that this is not currently AMP’s plan.

AMP’s strategic plan currently involves selling its life business which it hopes to realise $1.8bn. Other parts of its strategy involve slashing ‘Buyer of Last Resort’ (BOLR) contractual payments to its advisers by almost 40%. BOLR was a contractual arrangement where AMP would guarantee to buy an advisers business for 4 times recurring revenue.

It’s future strategy for resetting the culture of AMP wealth management includes terminating many of its advisers and offering a digital advice platform for certain client segments, while those advisers who will remain are to service ‘higher end’ clients.

AMP Capital, the funds management arm of the business is the jewel in the AMP crown. While it could operate on a stand alone basis, $116bn of the $200bn it manages comes from internal sources and this provided 30% of its income in the first half of 2019. The value of AMP Capital depends on the future of those funds.

Williams says “The major issue for us is whether the operational and cultural reset needed in AMP wealth management is just too big an ask. The new management team is untested against the mammoth task ahead.”

He adds, “We wonder whether a better outcome for shareholders might be a company led breakup of the whole business. We question whether the AMP brand in wealth management is salvageable and think board and management should re-test that hypothesis before going too far down the path of spending ~$1bn in re-setting the business.”

For the bears, Le Mesurier outlines 7 key risks.

- AMP now has an unsettled distribution force as a result of the reduction of the BOLR. The previously high multiple encouraged advisers to recommend AMP products to their clients. This issue possibly ends with a settlement involving further payments from AMP.

- The revenue margin decline in the wealth management business has been greater than management has expected for a number of years and this may continue to be the case.

- The revenue margin on the North product at 0.54% in first half of 2019 was less than the average cost of running the wealth management business which was 0.65%. North is the only product generating net inflows.

- The net cash outflows in the wealth management business are approximately 6% p.a. of Assets under management currently.

- The sale of the life insurance business has not been completed. It has failed once already and the price has been reduced.

- There is no guarantee that the expense reduction target will be met. The last time AMP attempted such a program, the costs increased.

- The customer remediation provisions may well be inadequate and they may face substantial litigation costs.

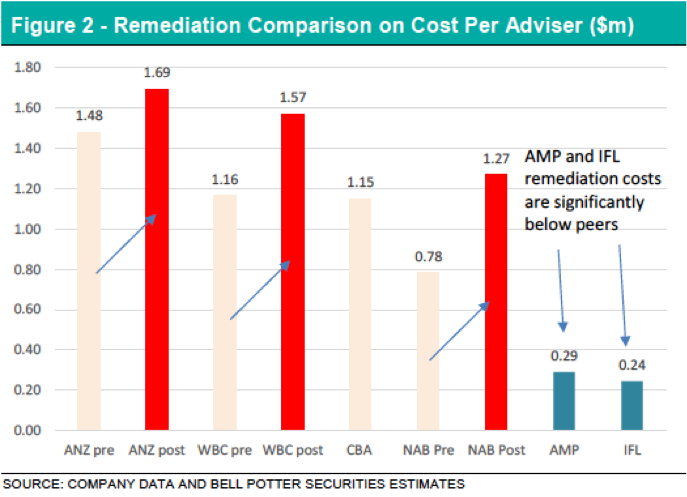

Le Mesurier adds “AMP’s remediation provisions seem to be inadequate in comparison with the actions taken by the major banks. The banks’ provisions are approximately double AMP’s and their adviser networks were much smaller and had a greater weighting towards salaried advisers. For AMP’s provisions to be adequate, their record keeping and the provision of advice would have to be much better than the major banks but their performance at the royal commission would not give confidence that was the case.”

The chart below, which includes the increase to remediation costs following the recent bank profit results, (red bars) shows the remediation costs measured per adviser. Should AMP’s cost per adviser rise to the level of ANZ, the additional cost for AMP shareholders could be north of $3bn.

The crucial time for the company and shareholders is when (if?) the life sale completes, and the accompanying investor update, but this turnaround is not for the faint hearted.

This article was written by Mark Draper (GEM Capital) and was featured in the Australian Financial Review in the week of 24th November 2019.