It’s now over a week since SpaceX made its Nasdaq debut and the parallels to the most reckless episodes in recent market history are impossible to ignore. On June 12 it launched at US$135 per share and surged more than 40% in two days. After a rollercoaster 11 days it is still up nearly 15%, and valued at around US$2.06 trillion, but well down from its highs.

It’s now over a week since SpaceX made its Nasdaq debut and the parallels to the most reckless episodes in recent market history are impossible to ignore. On June 12 it launched at US$135 per share and surged more than 40% in two days. After a rollercoaster 11 days it is still up nearly 15%, and valued at around US$2.06 trillion, but well down from its highs.

Beneath the spectacle something uncomfortably familiar is happening: the mechanics of a meme stock squeeze dressed up as the most exciting IPO in our generation.

The architecture of a squeeze

The SpaceX IPO was, by almost any measure, the largest in history. It raised US$75 billion, more than double Saudi Aramco’s 2019 record. What made it structurally unusual, however, was not the size but the design. Elon Musk’s team deliberately reserved approximately 30% of the offering for retail investors, routed through platforms including CommSec in Australia. The order book was rumoured to be 4x oversubscribed, with roughly US$300 billion in orders chasing the available allocation. Retail investors alone contributed an estimated US$15 billion of the raise, a number that Nasdaq’s own president described as larger than most IPOs he had seen.

The consequence of this design was predictable: most retail participants received only a fraction of what they requested. The artificial scarcity created by a deliberately constrained free float (Musk retains approximately 36% of the company himself, though controls 85%) means there is very little stock available for the enormous army of buyers who missed the IPO allocation and are now chasing the secondary market.

Enter the options market, which launched Monday on the Cboe. Where we have seen heavy retail buying in short-dated call options — the same lottery-ticket instruments that turbocharged GameStop’s infamous 2021 short squeeze. When retail traders pile into call options, market makers (who sell the options) must purchase the underlying shares to hedge their exposure. With a thin float and relentless buying pressure, this dynamic can create a self-reinforcing feedback loop that pushes the share price far above any rational assessment of value. After two days of options trading SpaceX share price hit an intra-day high of US$226 per share valuing the company at US$2.95 trillion. It’s difficult to know whether the current squeeze is over or is still in its early stages, with index buying expected to start next week.

What the market is missing

While SPCX absorbs the capital, the attention, and the oxygen of the financial media, there are global industry leaders trading at valuations that would have seemed extraordinary three years ago. Not because their businesses have deteriorated, but because they have simply fallen out of fashion.

Consider ResMed, the respiratory care giant which dominates the global CPAP therapy market with more than 15 million cloud-connected patients. In its most recent quarter, the company reported strong earnings growth of 10% year-over-year growth. EPS is forecast to grow approximately 30% over the next three years. The balance sheet has a billion dollars of net cash and a return on invested capital over 25%. And yet ResMed trades today at roughly 15x forward earnings, compared to its five-year historical average of nearly 29x. The stock sits near its 52-week low.

The cause of this dislocation is sentiment, not substance. Investors remain irrationally anxious about the long-term impact of GLP-1 weight-loss drugs on the sleep apnoea patient pool — a risk that the clinical evidence increasingly suggests is overstated. The data shows that demand for CPAP treatment has risen since the rise of GLP-1s, as diagnosis of sleep apnoea has increased.

Then there is Steadfast Group (a long-term holding in IML’s Funds). It is Australia’s largest general insurance broker network and an unambiguous leader in its industry, operating both broking and underwriting services. Like ResMed, Steadfast spent much of the past 12 months trading at deeply depressed valuation multiples, the victim of an increasingly fashionable anxiety: that artificial intelligence would disintermediate its industry and business model entirely, rendering human advice and broker relationships obsolete. Despite the market narrative, the business continued compounding. It is on track to deliver another solid year of earnings growth of 6-10%, yet the share price languished near A$4, an 11x multiple of earnings, a record low for the company compared to its 10-year average multiple of 20x. The market, preoccupied with disruption theory, had stopped paying attention to the actual business. Last week, a consortium comprising US wholesale insurance giant Amwins Group and San Francisco investment firm Dragoneer arrived with a takeover bid at $6 per share — a 52% premium to the prevailing share price. The market had set the stock aside: sophisticated global capital picked it up.

The oldest lesson in investing

History is littered with moments when the crowd was unified, confident, and catastrophically wrong: Japanese real estate in 1989; technology stocks at the peak of the dot-com bubble in 2000; US housing in 2006; GameStop in January 2021, when retail traders briefly pushed a failing video game retailer to a valuation that made no mathematical sense, only to watch it collapse by 90% within weeks.

None of this is to say that SpaceX will fail as a company. It very probably will not. Musk’s track record is not to be sneezed at. But there is an enormous difference between a great company and a great investment. The price you pay determines your return. At US$2 trillion, with no current earnings, a thin float, and an options market purpose-built for speculative excess, the risk-reward for new buyers of SPCX is deeply unfavourable.

Meanwhile, for Australian investors with a long-term orientation, the genuine opportunities lie elsewhere: in proven, profitable, cash-generative businesses that the market has set aside in its rush toward the spectacular. Companies with double-digit earnings growth, dominant competitive positions, and demonstrated pricing power are trading at the kinds of multiples typically associated with turnarounds rather than leaders.

The uncomfortable truth about investing is that the most rewarding positions are rarely the most popular ones. Buying what everyone wants, when everyone wants it, at the price everyone is willing to pay, is the surest path to mediocre returns. Buying what the crowd has discarded (a global respiratory care leader at 16x earnings, an overlooked insurance leader) when the narrative has soured, but the fundamentals remain intact, is where durable wealth is built.

SpaceX may one day justify its valuation over the decades to come. But in the near term, the mechanics of this IPO — the thin float, the retail frenzy, the options amplification — have created precisely the conditions that historically precede painful corrections in popular speculative assets.

The best investment decisions are often the least exciting ones.

This article has been reproduced with permission from Dan Moore - Investors mutual

The material is for general information only and does not take into account your personal objectives, financial situation or needs. You should consider, and consult with your professional adviser, whether the information is suitable for your circumstances.Statements of opinion are those of IML unless otherwise attributed. Except where specifically attributed to another source, all figures are based on IML research and analysis. Any investment metrics such as prospective P/E ratios and earnings forecasts referred to in this presentation constitute estimates which have been calculated by IML’s investment team based on IML’s investment processes and research. The fact that shares in a particular company may have been mentioned should not be interpreted as a recommendation to either buy, sell or hold that stock. Any commentary about specific securities is within the context of the investment strategy for the given portfolio.Any reference to a ranking, a rating or an award provides no guarantee for future performance results and is not constant over time.

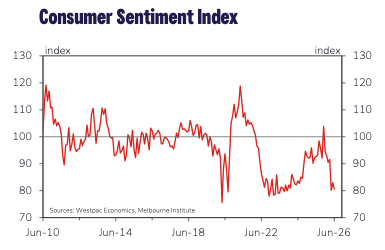

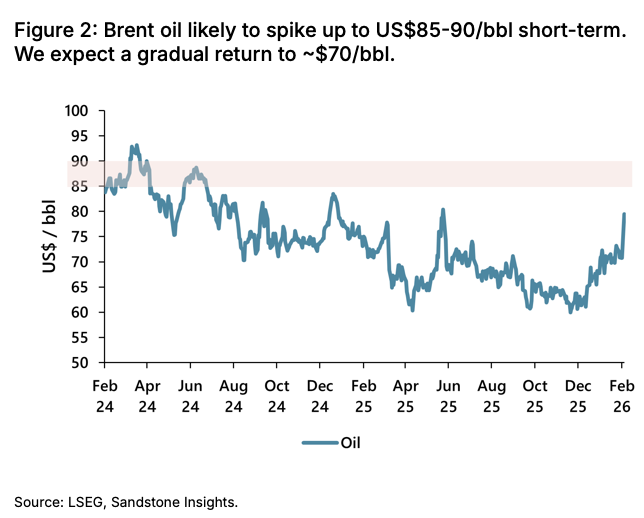

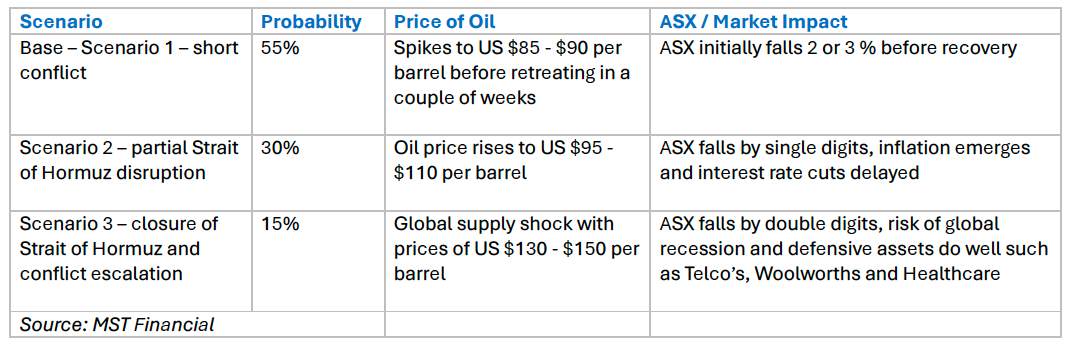

Over the weekend, tensions between the US, Israel and Iran escalated significantly following a coordinated strike by the US and Israel, which took out much of the Iranian leadership including the Supreme Leader.

Over the weekend, tensions between the US, Israel and Iran escalated significantly following a coordinated strike by the US and Israel, which took out much of the Iranian leadership including the Supreme Leader.

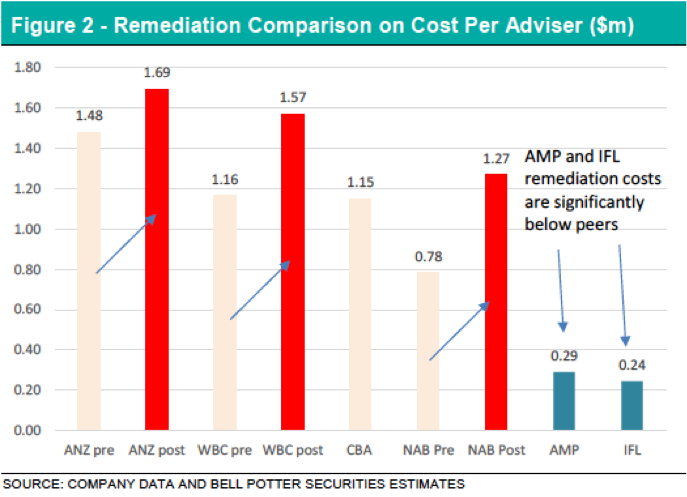

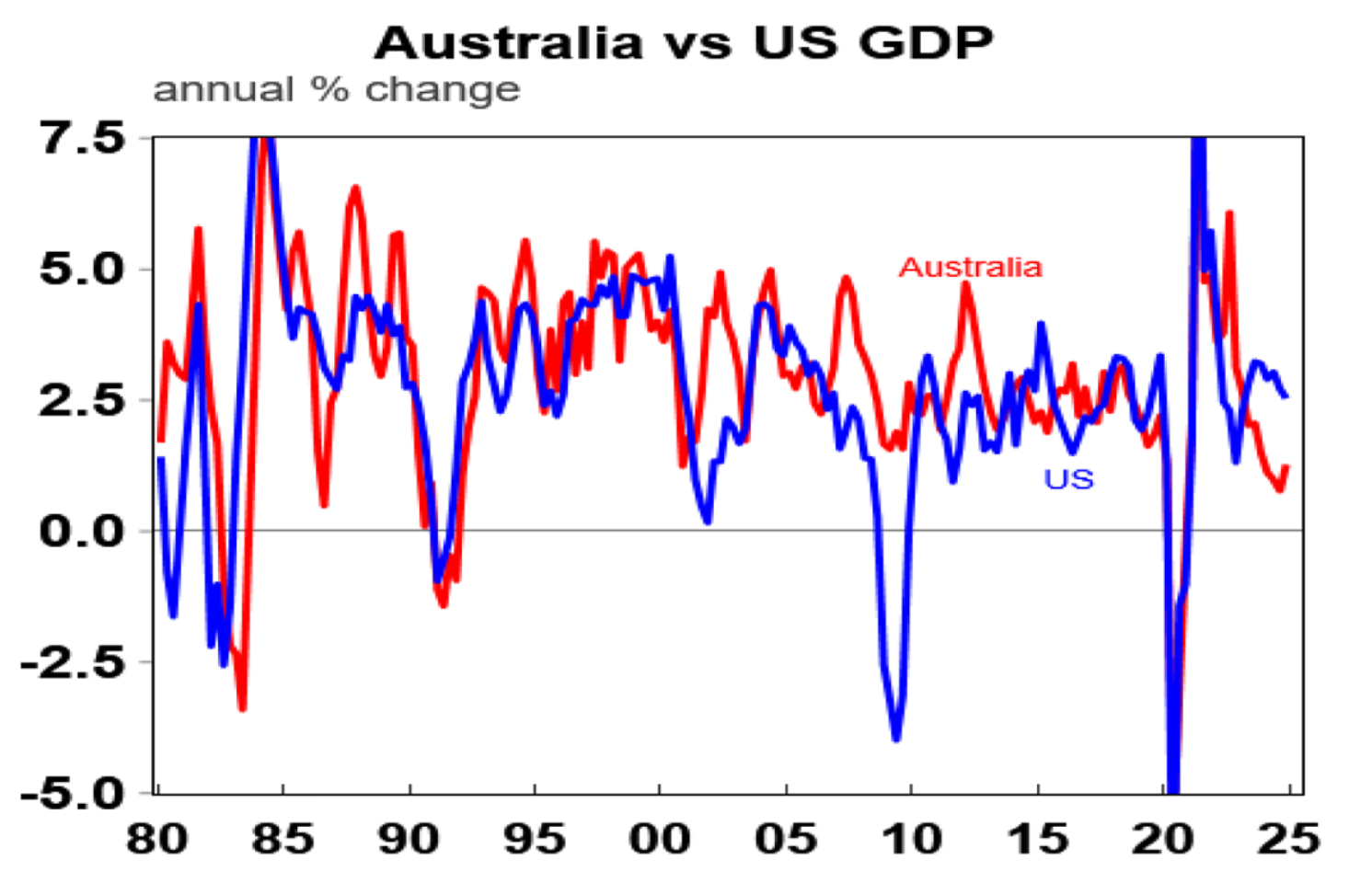

Westpac, NAB and ANZ have reported their annual results for the year ending 30th September 2024 and they all show that profit margins are under pressure and, despite nominal bad debts, profit growth remains elusive. How then to explain the record valuations of this group, not to mention CBA which is the most expensive bank in the world.

Westpac, NAB and ANZ have reported their annual results for the year ending 30th September 2024 and they all show that profit margins are under pressure and, despite nominal bad debts, profit growth remains elusive. How then to explain the record valuations of this group, not to mention CBA which is the most expensive bank in the world.

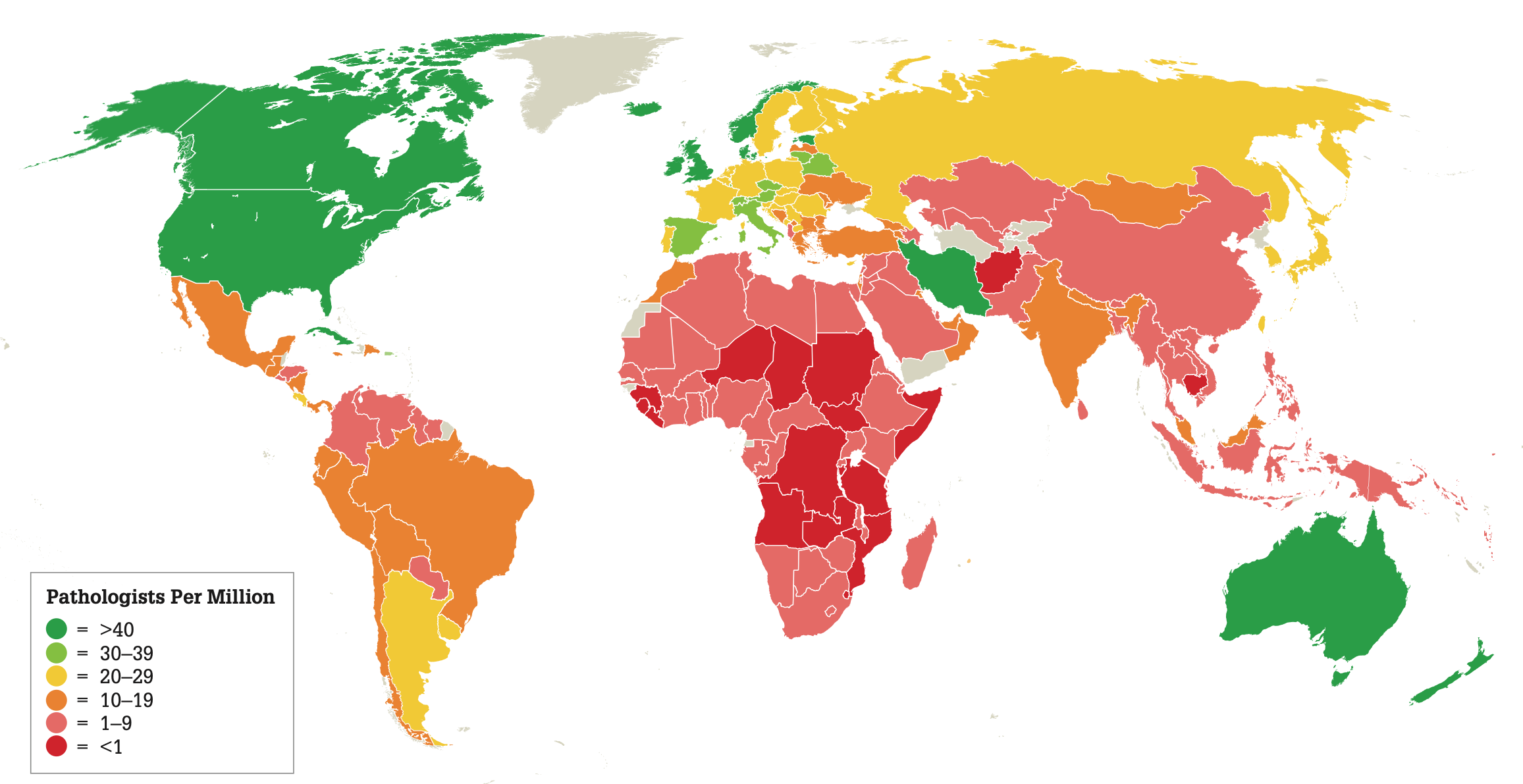

The current share prices of all 3 Australian listed pathology companies are below pre-COVID levels. In Sonic’s case, this is despite earnings per share in financial year 2023 being 19% higher than that in the 2019 financial year. Investors should ask themselves whether this represents a buying opportunity.

The current share prices of all 3 Australian listed pathology companies are below pre-COVID levels. In Sonic’s case, this is despite earnings per share in financial year 2023 being 19% higher than that in the 2019 financial year. Investors should ask themselves whether this represents a buying opportunity.

Artificial Intelligence, known as AI has been a hot sector so far in 2023. Computer chip designer Nvidia Corp, the current poster child of AI, has seen its share price rise around 200% this calendar year, while Microsoft is up around 50% so far this year.

Artificial Intelligence, known as AI has been a hot sector so far in 2023. Computer chip designer Nvidia Corp, the current poster child of AI, has seen its share price rise around 200% this calendar year, while Microsoft is up around 50% so far this year.

Warren Buffett’s two golden rules for investing are, 1. Don’t lose money 2. Never forget rule one.

Warren Buffett’s two golden rules for investing are, 1. Don’t lose money 2. Never forget rule one.