Following the most savage sell off in REIT’s since GFC, investors are left to decide whether to buy the lower prices or sell on the basis that COVID-19 has forever changed property.

During the month of March, the REIT’s index fell 35%. While the sector fared worse during GFC, this sell off has been fast and brutal.

Investors need to understand that not all REIT’s are created equal and they generally fall into 3 sectors:

- Retail

- Office

- Industrial

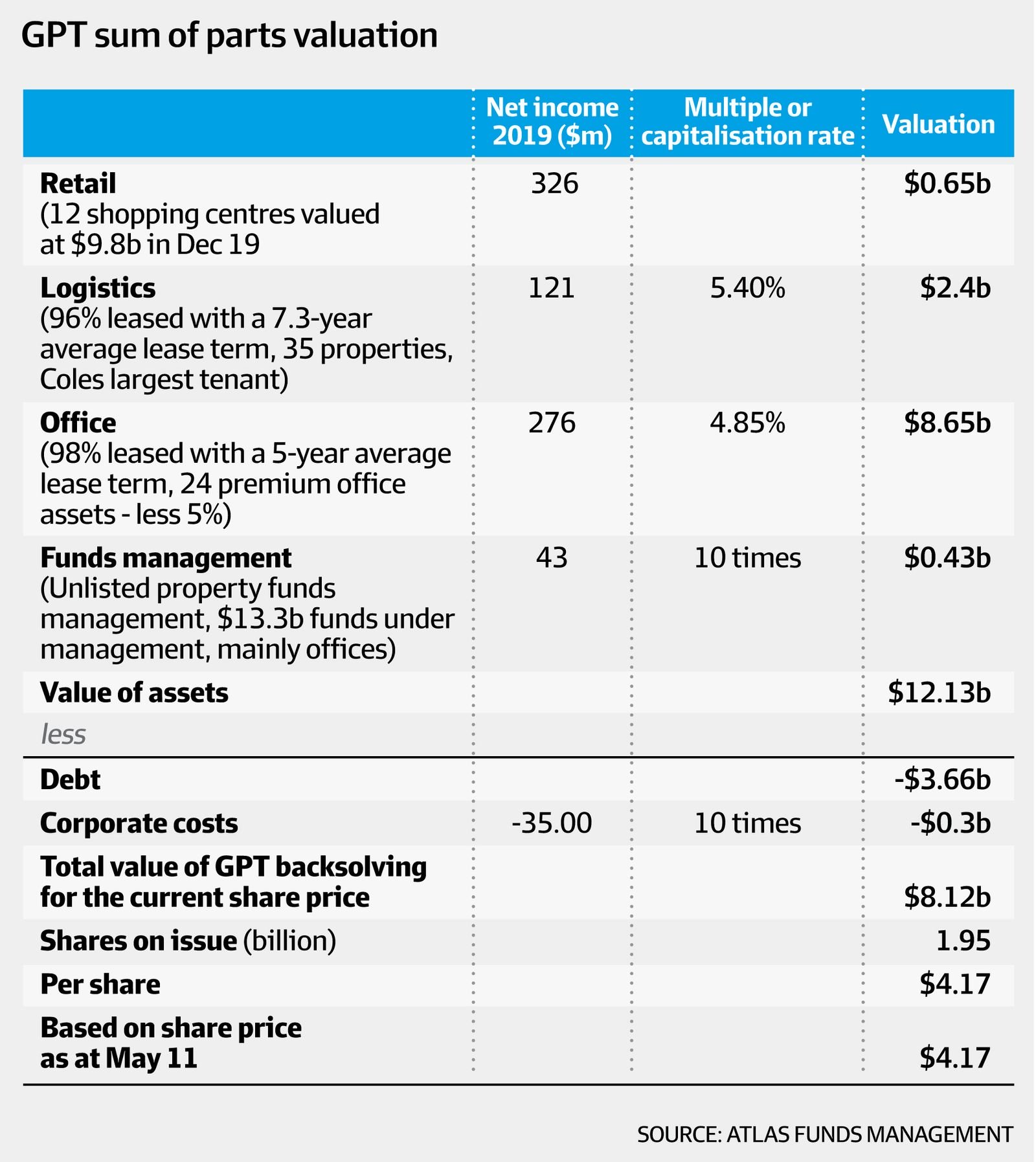

One of the major risks for property investors is vacancies and COVID-19 may cause vacancies through business bankruptcies. The retail property sector is at the epicentre of this risk. This risk would appear to be in current prices and Hugh Dive (Portfolio Manager Atlas Funds Management) is of the view that “some of the sentiment towards retail appears excessively bearish.” He makes this point by backsolving the current share price of GPT Group’s property portfolio of retail, office and industrial assets.

The table below shows that at current prices, GPT investors are assigning GPT’s 12 shopping centres a value of $650 million. According to Dive “this appears to be unlikely for a collection of assets that generated profits of $326 million last year. If you demolished the shopping centres, the land value is most certainly worth a lot more than this.”

Pete Morrissey (CEO Real Estate Securities, APN Property Group) says that “COVID-19 is a catalyst to speed up the tenant turnover/bankruptcy and rent reversion cycle that was likely to continue for several more years into a compressed period. While this may bring pain to landlords and tenants it could also see the emergence of a more vibrant, customer focussed retail sector. Those properties that are well located with owners focused on meeting consumer needs will continue to drive solid return outcomes once markets stabilise.”

Dive summed up his views on retail property with “human beings have consistently enjoyed shopping and dining in public areas for two and half thousand years since the agora was built in Athens in the Fifth CenturyBC and it is hard to make the case that COVID-19 in 2020 totally changes that behaviour”.

A common theory with office space is that COVID-19 will permanently change the demand profile for office space as companies move their employees toward working from home.

Morrissey says “While we don’t disagree entirely with this we do question whether corporates will be willing to forego the obvious gains from staff networking efficiencies and personal interactions/collaborations across their organisations.” He also introduced the prospect that tenant space savings from staff working at home could be offset by social distancing requirements being introduced to the office.

Dive believes “that COVID-19 will reduce the demand for office space and rents will fall, but we don’t see a fundamental decline in value of office real estate.” This is largely due to the tight vacancy rates in Sydney and Melbourne that should provide some support to rents over the coming years.

Industrial property would seem to be the most insulated sector from the impact of COVID-19.

“Industrial property, in particular logistics is likely to see a minimal impact from COVID-19 as their tenants are likely to see solid demand through 2020” according to Dive.

Morrissey agrees and adds “increasing infrastructure spending, growing e-commerce, and a renewed focus on shoring up local supply chains will be an ongoing tailwind to drive industrial property demand. Low vacancy rates across the sector indicate that industrial property is not over-supplied”.

Those investors who remember the highly dilutionary capital raising’s from REIT’s during GFC should take comfort in the low gearing of the sector today. Average gearing today is around 28% compared to GFC levels of around 40%. Dive is of the view that while we have seen a few small opportunistic capital raisings in 2020, we are unlikely to see a large number of jumbo ‘life or death’ capital raisings in the REIT sector like we saw during GFC.

Investors can gain access to REIT’s by either purchasing them directly via the ASX, or through diversified property funds such as those offered by Atlas Funds Management and APN Property Group. ETF’s are another way of gaining property exposure, but investors should be aware that the property index is dominated by retail property if choosing to index their property exposure.

It is said that it is always darkest just before the dawn. Long term investors could well make good long term returns from sifting through the REIT wreckage.

This article was written by Mark Draper (GEM Capital) and was published in the Australian Financial Review on Wednesday 13th May 2020.