Some of the best investment ideas come from observing daily life. Smartphones have around 90% penetration rate in Australia (statista.com) which has resulted in many profitable investments including Apple, Facebook, REA and Life 360 just to name a few.

Doctor’s visits are a normal part of life for most people. Pathology tests are a natural consequence of visiting a doctor, and this sector too is investable.

Outside of the COVID pandemic, the proportion of Australians accessing pathology services is relatively constant at around 55%. This means that growth in tests is likely to come from population growth and the ageing of the population. This can be seen in the graph below which shows the growth in pathology in Australia in recent years.

Worldwide, the number of people aged over 60 is forecast to double to 2.1bn by 2050. As a statement of the obvious, as people age, the chances of contracting illness increases dramatically. The National Cancer Institute says that those over 60 are around 40 times more likely to develop cancer than young people in their 20’s. Pathology is required 100% of the time to diagnose cancer.

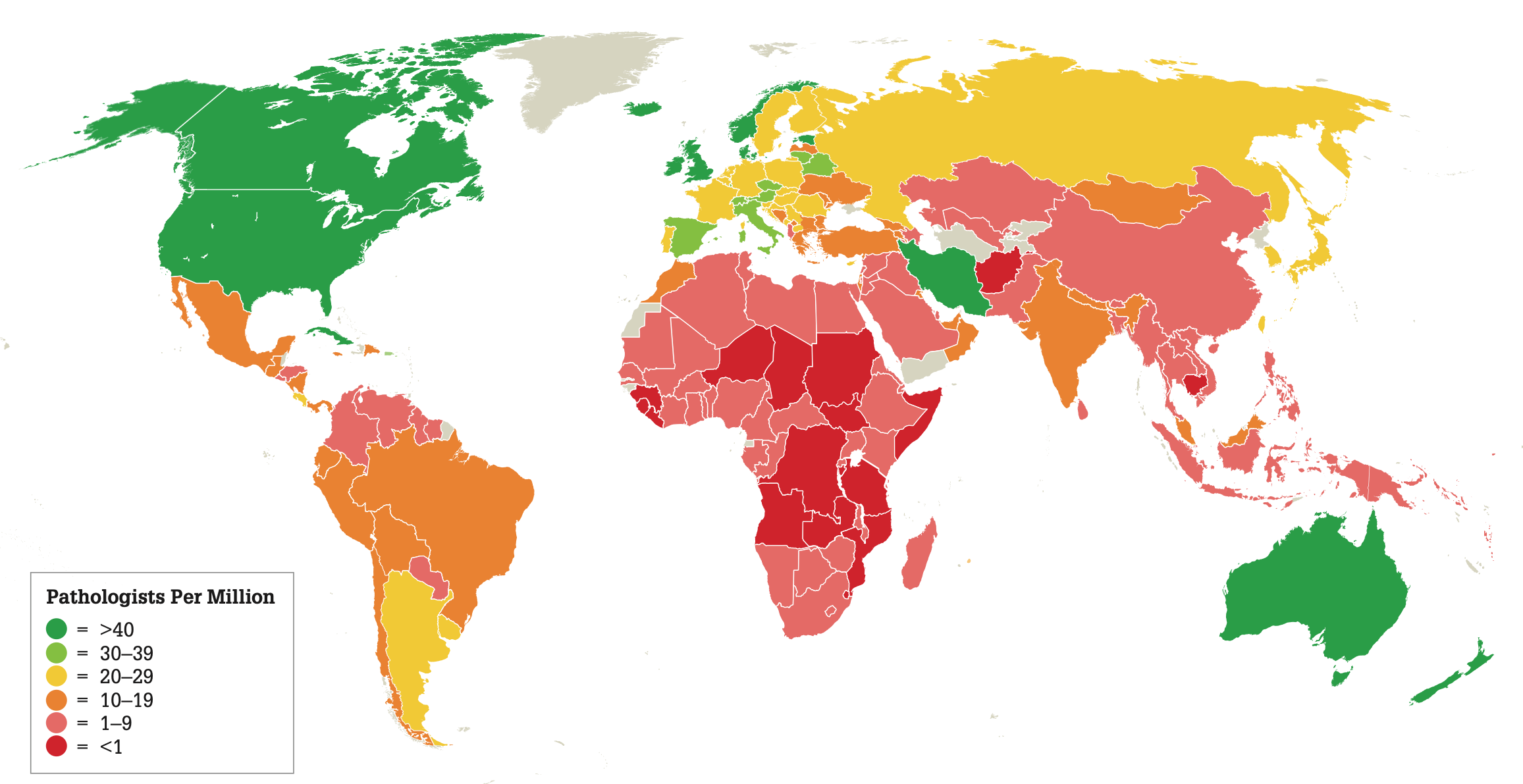

Developing countries also present a growth opportunity to the pathology sector as those countries embrace Western medicine. This can be seen in the world map which shows the number of pathologists per million people. The orange, pink and red coloured regions show countries that are not well represented by pathology services.

Source: Thepathologist.com

Source: Thepathologist.com

In Australia there are 3 listed pathology companies, Sonic Healthcare (which also operates in Europe, UK and the US), Healius and ACL. Sonic has a market capitalisation of $12.8bn, Healius $936m and ACL has a market capitalisation of $500m.

Our preferred investment in the pathology sector is Sonic Healthcare which locally operates under the brand name Clinpath. Scale matters when it comes to pathology as the more tests that can be completed by your existing network results in higher return on capital.

Sonic, as the largest player in the market can also afford to heavily invest into the future. Sonic has invested into technology required to make it the dominant pathology provider for telehealth which has dramatically increased in size since the pandemic.

The other area Sonic is heavily investing in is Artificial Intelligence (AI) where it has invested $350m over the last two years.

Sonic owns 49 per cent of Franklin.ai, its joint venture with Harrison.ai. Through another joint venture, Annalise.ai, Harrison.ai has developed AI models for interpreting brain scans and chest X-rays, already available to one third of radiologists in Australia and clinics in APAC, Europe, UK, Middle-East and the US. These developments should allow pathology providers to complete a larger number of tests using the same resources. Sonic may also have the option to sell this technology to other pathology companies. Sonic management have said they expect AI to make a material improvement to future earnings.

The other area where AI has potential to be transformative is in the histopath part of the business which involves the testing of tissue. This is currently a manual process with pathologists viewing tissue samples through a microscope in order to diagnose. Sonic has acquired Pathology Watch which provides a laboratory information system, digital pathology viewer, image storage and AI algorithms. This allows high quality digitised whole slide images to be accessed and reported by a pathologist wherever they are located. This allows images from multiple sites to be distributed to pathologists in any location to balance workloads and speed up expert second opinions. Additionally, the use of AI can help to further increase the efficiencies of pathologists and improve turnaround times.

The pathology sector typically grows its revenues by 3 – 5%pa and recently Sonic reported in May 2024 that their revenue had increased 6% in the 2024 financial year to date. Included in this announcement was a minor profit downgrade for this financial year due to higher costs which is largely due to the residual of COVID testing. These expenses are anticipated to cease at the end of calendar 2024.

The current share prices of all 3 Australian listed pathology companies are below pre-COVID levels. In Sonic’s case, this is despite earnings per share in financial year 2023 being 19% higher than that in the 2019 financial year. Investors should ask themselves whether this represents a buying opportunity.

The current share prices of all 3 Australian listed pathology companies are below pre-COVID levels. In Sonic’s case, this is despite earnings per share in financial year 2023 being 19% higher than that in the 2019 financial year. Investors should ask themselves whether this represents a buying opportunity.

Sonic’s balance sheet is strong with net debt to equity ratio of around 40%, while ACL’s is 170% and Healius has net debt to equity of over 140% (source Stockdoctor.com).

Investors are being offered a gross forecast dividend in 2025 of 5% from Sonic, 6.4% from ACL and below 2% from Healius. (source Stockdoctor.com)

The key risks in the pathology sector are changes to Government funding policy and technological advances that could render third party pathology tests obsolete.

The pathology sector though is a business with stable revenue growth and upside potential from AI, the ageing of the population and additional tests from developing countries in time. Investors should examine it under the microscope.