Key points

- After recent sharp falls the $A may see a short-term bounce, but the broad trend is likely to remain down against the $US reflecting a rising $US generally, a secular downswing in commodity prices, overvaluation in terms of relative prices and monetary tightening in the US relative to Australia.

- So while the $A may consolidate into year end, it's expected to see another leg down next year taking it to around $US0.80.

- The downtrend in the $A is good news for the local economy and share market (via a boost to earnings), but along with the downtrend in commodity prices highlights the case for global investments in foreign currencies.

Introduction

The past month has seen a sharp fall in the value of the Australian dollar from around $US0.94 to a low of near $US0.86. While there will be short term gyrations, the broad trend in the $A likely remains down. This is part of a bigger global shift involving a stronger $US.

A secular upswing in the $US

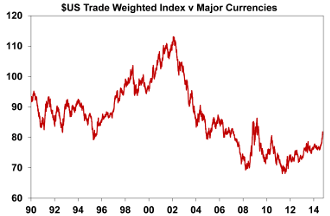

Not only has the Australian dollar fallen sharply against the $US recently but so too have currencies such as the Euro and Yen. The chart below shows the value of the $US against a trade weighted basket of major currencies.

Source: Thomson Reuters, AMP Capital

The $US has been tracing out a broad bottom since 2008. This is likely part of a broader long term or secular pattern:

- During the second half of the 1990s the $US surged in value as the US was seen as a global growth and innovation leader.

- During last decade from 2002 the $US traced out a broad decline as emerging market countries were much stronger.

- But since the GFC the $US seems to be bottoming. Our assessment is that the secular downtrend in the $US since 2002 is now over and that it will now trend higher.

Because the US was proactive in dealing with the GFC its economy is now on a sounder footing globally and, like in the 1990s, it’s becoming something of a growth locomotive again:

- The Fed will soon end its quantitative easing program and may start to raise interest rates next year.

- But there is no end in sight for the Bank of Japan's bigger money printing program and the European Central Bank is about to embark on its own QE program this month. Neither is even contemplating raising interest rates.

- While China is still strong its pace of growth has slowed with its own structural issues and pressure on the People's Bank of China to ease monetary policy. What's more the bulk of the rise in the Renminbi is likely behind us.

- The emerging world is now beset by various structural problems which will possibly constrain their growth.

All of this points to a longer term upswing in the $US. This has a number of implications including less pressure on the Fed to raise rates as a rising $US is a de-facto monetary tightening (so lower US interest rates for even longer) and downwards pressure on commodity prices. In many ways it looks like we could be seeing a re-run of the second half of the 1990s which saw the US as the world's locomotive, a strong $US, weak commodity prices, benign inflation, relatively low interest rates and strong gains in US shares

A secular downswing in commodity prices

Just as the $US appears to be embarking on a long term upswing, commodity prices look to be in a long term down swing. In fact they are related as there are two drivers of the trend in commodity prices:

- Supply and demand. Last decade demand for industrial commodities was surging led by industrialisation in China as supply (after years of commodity weakness) struggled to catch up. Now it’s the other way around as demand growth in China while still strong has slowed (accentuated by a cyclical downturn in property related demand) and supply is surging after record investment in in sources for everything from coal and iron ore to gas.

- The value of the $US. Since commodities are priced in US dollars they move with it. They rose last decade when the $US was in decline and are now heading down as the $US is on the way up.

As can be seen in the next chart raw material prices trace out roughly 10 year long term upswings followed by 10 to 20 year long term bear markets. After an upswing last decade, they now look to be embarking on a secular downtrend.

Source: Global Financial Data, Bloomberg, AMP Capital

..and a secular downswing in the $A

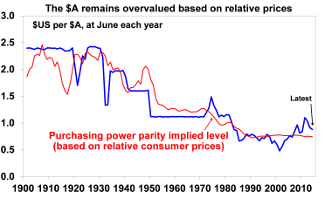

Against this backdrop the big picture outlook for the $A is not flash. First, it's best to start with what economists call purchasing power parity, according to which exchange rates should equilibrate the price of a basket of goods and services across countries. A guide to this is shown below which shows the $A/$US rate (against where it would be if the rate had moved to equilibrate relative consumer price levels between the US and Australia since 1900.

Source: RBA, ABS, AMP Capital

Purchasing power parity doesn’t work for extended periods. But, it does provide a guide to where exchange rates are headed over long periods of time. Right now on this measure the $A is still 15-20% overvalued, with fair value around $US0.75. This also lines up with anecdotes of high prices and labour costs in Australia compared to other countries.

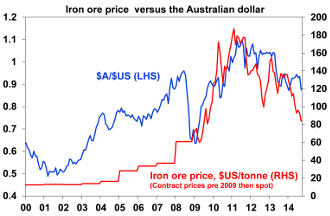

Second, as already noted, commodity prices are in a secular downswing. This is highlighted by the iron ore price which a decade ago was around $US20/tonne rose to $US180/tonne in 2011 and has since fallen back to around $US80/tonne.

Source: Bloomberg, AMP Capital

Third, while Australian interest rates are still above those in the US and elsewhere the gap has narrowed. Moreover the Fed in the US is soon to end its monetary stimulus program and is likely to start raising interest rates well ahead of the RBA.

Fourthly, perceptions of global investors about the $A appear to be changing. Over much of the last decade it was positive reflecting Australia’s favourable fundamentals tied to growth in the emerging world and more latterly as an AAA rated safe haven. Now there is a bit more wariness as emerging markets have gone out of favour and if Australia fails to get its budget deficit under control (with Senate blockages and the fall in the iron ore price likely to result in another deterioration in the next MYEFO budget outlook due later this year) foreign perceptions could deteriorate further.

Finally, as already discussed the trend in the $US is likely to be up.

In the short term, the Australian dollar has fallen a bit too far too fast (just as the $US has risen too far to fast), so a short covering bounce could well emerge over the next month or so. Indeed the $A seems to be finding support around $US0.8640.

However, for the reasons noted above the broad trend in the $A is likely to remain down. I remain of the view that it will fall to around $US0.80 in the next year or so as the Fed eventually starts to raise interest rates, with the risk of an overshoot on the downside.

Of course it's worth noting that the fall in the $A on a trade weighted basis won’t be as pronounced as against the $US as major currencies like the Yen and Euro are also likely to fall against the $US.

Implications for investors

There are a several implications for investors.

First, the fall in the $A back towards more fundamentally justified levels is good for the Australian economy and ultimately the local share market. When the $A is in free-fall it is often bad news for the Australian share market as foreign investors retreat to the sidelines for fear of losing more of their money. But after a while the lower $A will become a source of support for the market as it flows through to upwards revisions to earnings expectations. A rough rule of thumb is that each 10% fall in the value of the $A boosts company earnings by 3%. Providing the downtrend in the $A remains gradual the negative impact from the boost to inflation flowing from higher import prices should remain modest.

Second, and perhaps more significantly, the outlook for a continuing downtrend in the value of the Australian dollar highlights the case for Australian based investors to have a relatively greater exposure to offshore assets that are not hedged back to Australian dollars (ie remain exposed to foreign currencies) than was the case say a decade ago when the $A was in a strong rising trend. Put simply, a declining $A boosts the value of an investment in offshore asset denominated in foreign currency 1 for 1. Eg a 10% fall in the value of the $A will boost a foreign share portfolio by 10% in value in Australian dollar terms.

Finally, the longer term downtrend in commodity prices also works in favour of having a relatively greater exposure to traditional global shares as the US, Europe and Japan are commodity users and tend to benefit from softer commodity prices whereas it’s a headwind for the Australian economy.

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital

- See more at: http://media.amp.com.au/phoenix.zhtml?c=219073&p=irol-oliverArticle&ID=1977737#sthash.cA0gY2CL.dpuf