The Government recently released its Intergenerational report which occurs once every 5 years. The report is designed to provide Government with a basis in which to formulate long term policy (one must be careful not to laugh out loud at this point).

One of the glaring aspects of this report revolves around the ageing of Australia's population and here we provide some of the charts contained in the Intergenerational Report that highlight this ageing profile.

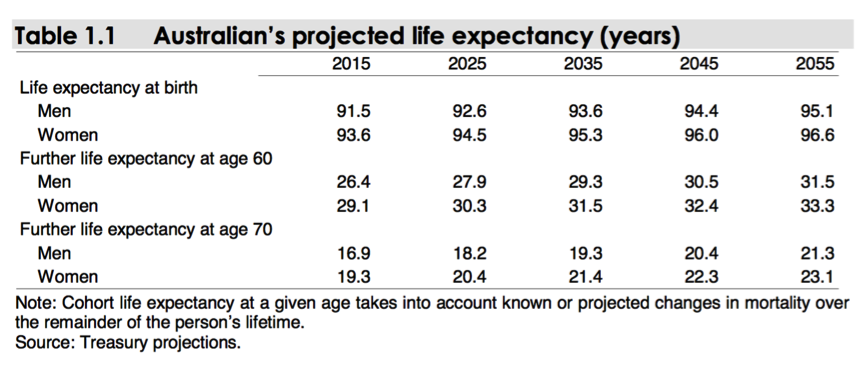

First the good news, which is on average we are going to be living longer.

Some key points from this table are that males born now can expect to reach 91.5 years old, but in 40 years they should expect to live until over age 95. From a retirement perspective, those men who reach the retirement age of 60 currently can expect to live for a further 26.4 years (29 years for women), but in 40 years time it is expected that a 60 year old male will have over 31 years in retirement (over 33 years for women).

This tells us that people are going to have to save more for retirement as they are likely to be living longer in retirement. Joint replacements are going to be in huge demand as the body will be required to last longer than at anytime in modern history. Divorce rates may increase as those who reach retirement will have over 30 years to live whereas in 1975, their retirement years were likely to be almost half, resulting in people staying together unhappily because 'there's not much time left anyway'.

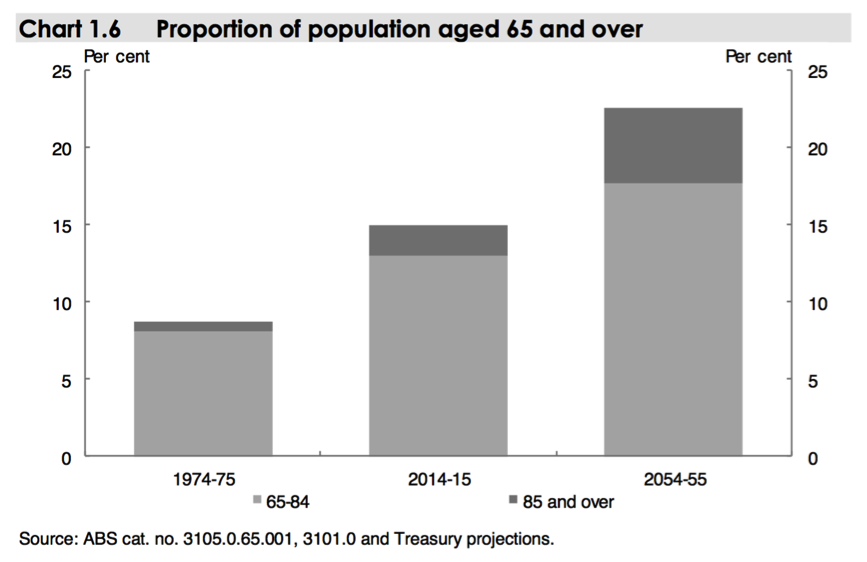

The proportion of the population of those over age 65 is going to materially increase which can be seen in the next chart, and of particular interest (from a medical expense perspective) is the growing band of over 85 year olds.

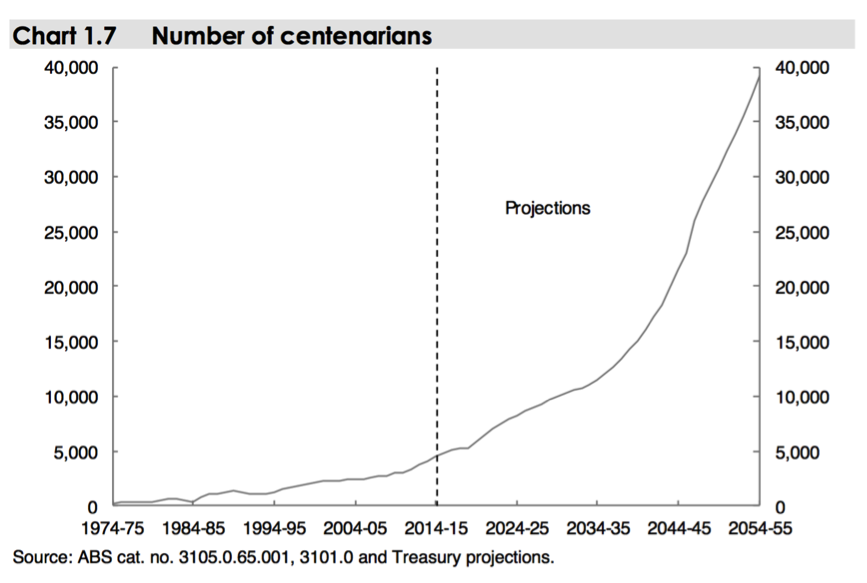

From a different viewpoint, the future number of people living beyond 100 years is going to put pressure on the Royal Family and our politicians to recognise 100th birthdays as the number of centenarians is forecast to grow from under 5,000 today to almost 40,000 by 2055. Perhaps 100 will be the new 80?

Finally, and one of the most hard hitting chart is the one that shows how many people of working age 15-64 will exist to support those over the age of 65. In 1975 there were 7.3 people aged between 15-64 (assumingly paying taxes and working) to support 1 person over the age of 65 (who had a relatively short life expectancy by today's standard).

In 2025 that number will fall to 3.7 people aged between 15-64 supporting one person over the age of 65.

It is forecast that by 2055, the number of working people will fall to 2.7 persons for every person over the age of 65.

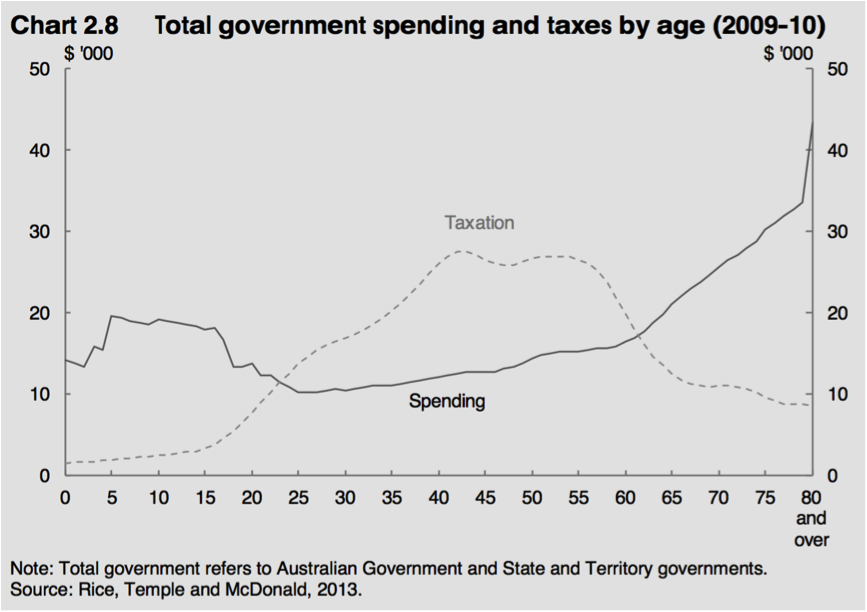

This is critical as the level of Government spending per person is at its peak for those over age 65, as it allocates money for age pension payments and also for medical expenditure. So Government spending is potentially in for a triple whammy in that there is forecast to be

1. a higher proportion of the population over 65 which contribute less tax but cost more,

2. those over age 65 are forecast to live longer, so not only do they cost the Government more, but will cost more for longer

3. the number of people in the workforce compared to those retired is forecast to drop dramatically - and those working are likely to be unhappy if taxes rise to support the retiree population.

You will also note from the chart below, that spending on children is also high, although not as high as those over 65, as Government spending comes in the form of education costs (largely).

Ablert Einsten's definition of insanity was to "keep doing the same thing over and over, and expect a different result". We would argue that many government policies in the area of healthcare, taxation and welfare were structured decades ago, and if Australia continues to do the same things over and over in light of the population changes that are forecast, then we are insane.

Government policy is going to have to change to meet the demands of the changing nature of Australia's population.

Investors will need to consider this, particularly when investing in businesses that are partly funded by Government (read healthcare) as government priorities and spending ability will most certainly change over time.

Investors should also turn their mind toward some of the other effects of an ageing population with respect to demand for things that retirees seek such as travel, healthcare and demand for financial services. There is also very likely an impact on the residential property market when retirees look to downsize their houses.

We encourage readers to look at the intergenerational report, not that we expect much in the way of action from the current political leaders in the short term, (from all sides of politics), but at some stage Australia is going to have to position itself for these changes.