Key points

- The mining investment boom still has another year or two to go but its peak is starting to come into sight and the best has probably been seen in terms of commodity prices.

- While there is the risk of a timing mismatch around the end of the investment boom in 2014 and as other sectors take over in driving Australian economic growth, the eventual end of the mining investment boom should lead to more balanced Australian growth.

- The eventual slowing of the mining boom should mean lower interest and term deposit rates, the best is over for the Australian dollar (A$) and a more balanced share market.

Introduction

Recent weeks has seen much debate and consternation in Australia as to whether the mining boom that has supposedly propelled the economy for the last decade is over. This followed the cancellation or delay of various resource investment projects including the massive Olympic Dam expansion and a fall in commodity prices over the last year.

But is it really over? And would it really be the disaster for Australia that many fear? After all, we have had years of hearing about the two-speed economy where the less resource-rich south eastern states were being left behind and it was said that the people of western Sydney were paying the price (via higher-than-otherwise interest rates and job losses) for the boom in Western Australia, so many Australians might be forgiven for thinking good riddance.

Semantics and confusion

Much of the debate about whether the mining boom is over has been characterised by confusion as to what is being referred to with some focusing on commodity prices, others on mining investment projects and others saying that technically it hasn’t even begun until mining and energy exports pick up. In broad terms the mining boom that has gripped Australia for the last decade likely has three stages.

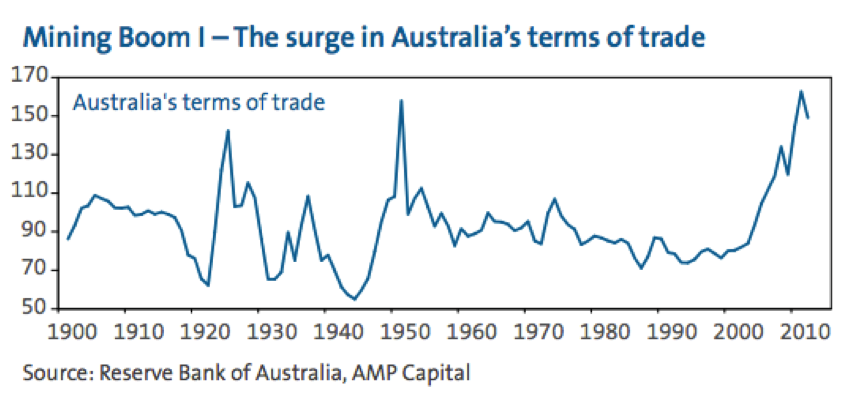

The first stage, or Mining Boom I (MB I), began last decade and saw surging resource commodity prices driven by industrialisation in China. This resulted in a rise in Australia’s terms of trade to near record levels (see the next chart). This phase was initially good for

Australia last decade as it seemingly benefited everyone. Resource companies got paid more for what they produced, their profits surged, they employed more people, and they paid more taxes, which led to budget surpluses and allowed annual tax cuts. They paid more dividends and their share prices went up. The A$ rose but not to levels that caused huge problems for the rest of the economy. So, not only did the resources companies benefit but there was a big trickle down effect to almost everyone else. As a result the economy performed very strongly and unemployment fell below 4%.

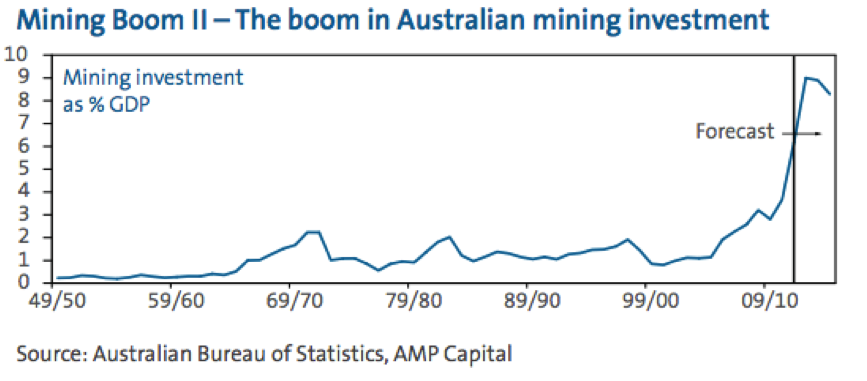

The second stage, or Mining Boom II (MB II), has been characterised by a surge in mining and energy investment. This has been underway for the last few years and will take mining investment from around 4% of gross domestic product (GDP) in 2010 up to around 9% in 2013, contributing around 2 percentage points to GDP growth in each of 2011-12 and 2012-13.

The third stage, or Mining Boom III (MB III), will presumably come when resource exports surge on the back of all the investment. So where are we now? In terms of the commodity price surge that characterised MB I, it’s likely that we have either seen the peak or the best is over with more constrained gains ahead:

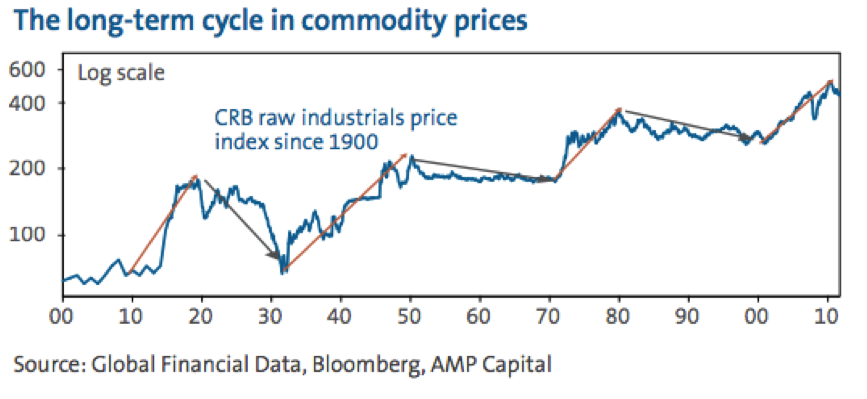

- Firstly, the pattern for raw material prices over the past century or so has seen roughly a 10-year secular or long-term upswing followed by a 10- to 20-year secular bear market, which can sometimes just be a move to the side.

The upswing is normally driven by a surge in global demand for commodities after a period of mining underinvestment. The downswings come when the pace of demand slows but the supply of commodities picks up in lagged response to the price upswing. After a 12-year bull run since 2000 this pattern would suggest that the commodity price boom may be at or near its end.

- Global growth appears to have entered a constrained patch. Excessive debt levels in the US, Europe and Japan have constrained growth, while potential growth in China, India and Brazil looks like being 1 or 2 percentage points lower than was the case before the global financial crisis. This means slower growth in commodity demand going forward.

- The supply of raw materials is likely to surge in the decade ahead in response to increased investment.

- Finally, the surge in commodity prices since 2000 was given a lift by a downtrend in the US dollar from 2002 as commodity prices are mostly priced in US dollars. This has now likely largely run its course.

Taken together, this would suggest that the best of the commodity price surge since 2000, or MB I, is behind us. There are two qualifi cations though. First, after the recent short-term cyclical slump there will still be a rebound, probably into next year as global growth picks up a bit. Second, it’s way too premature to say that the surge in demand in the emerging world is over - China and India are still very poor countries with per capita income of just US$8,400 and US$3,700 respectively compared to US$40,000 in Australia suggesting plenty of catch-up potential ahead and related commodity demand.

In terms of MB II, while the cancellation of Olympic Dam and other marginal projects indicates that projects under consideration have peaked, this does not mean the mining investment boom is over. In fact it probably has another one to two years to run. Based on active projects yet to be completed there is a pipeline of around A$270 billion of work yet to be completed. Iron ore related capital spending (on mines and infrastructure) are likely to peak this fi nancial year and coal and liquid natural gas related investment is likely to peak in 2014-15, suggesting a peak in aggregate around 2014.

In other words, the boom in mining investment has 18 months or so to run before it peaks and starts to subside back to more normal levels. But what can be said though, is with the cancellation of marginal projects that were in the preliminary stage, the end is coming into sight.

Finally, MB III or the pick-up in export volumes flowing from the surge in mining investment in iron ore, coal and liquefied natural gas will start to get underway around 2014-15.

Heading towards a more balanced economy

Talk of the end of the mining boom has created a bit of nervousness regarding the outlook for Australia. However, the reality is that the current stage of the mining boom focused on

mining investment has not been unambiguously good for the economy and its inevitable end should hopefully see Australia return to a more balanced economy.

It was always thought that after two or three years the surge in mining investment would settle back down as projects ran their course. Trying to do a whole lot of projects in a relatively short space of time was always fraught with the threat of excessive cost

pressures and an excessive surge in supply. We are now seeing market forces kicking in to rationalise resource projects and so the more marginal projects are being delayed. This is a good thing as it will reduce cost pressures, leave work for the future and reduce the

size of the commodity supply surge over the decade ahead thereby helping avoid a crash in commodity prices.

The cooling down of the mining investment boom should help lead to a more balanced economy. MB II has not been good for big parts of Australia. With roughly 2 percentage points of growth coming from mining investment alone it has really put a squeeze on the

rest of the economy. Housing and non-residential construction, retailing, manufacturing and tourism have all suffered under the weight of higher-than-otherwise interest rates and a surge in the A$ to 30-year highs.

What’s more the boom in mining investment has meant that the Federal Government has not seen the tax revenue surge it got last decade, so last decade’s regular tax cuts have not been possible and this has weighed on household income.

This is all evident in the Australian share market which has underperformed global shares since late 2009, with the resource sector being the worst performer over the last year as resource sector profits have fallen 15% or so.

So, the end of the mining investment boom, to the extent that it takes pressure off interest rates and the A$, should enable the parts of the economy that have been under the screw for the last few years to rebound, leading to more balanced growth. This is also likely to be augmented by a pick-up in resource export volumes equal to around 1% of GDP from around 2014-15 according to the Bureau of Resource and Energy Economics.

Of course a risk is of a timing mismatch around 2014 as investment slows down with other sectors taking a while to pick up. To guard against this the Reserve Bank will clearly need to stand ready to respond with lower interest rates.

The bottom line is that the end of the mining investment boom in a year or two won’t necessarily be bad for the Australian economy and will likely see a return to more balanced growth.

Concluding comments

It’s premature to call the end of the mining boom just yet. The peak in mining investment probably won’t be seen until 2014 and thereafter actual mining production and hence exports will start to pick up. However, the best has probably been seen in terms of commodity price gains and the end of the investment boom is starting to come into sight.

While there may be the risk of slower growth as the Australian economy shifts gears away from mining investment in 2014 to mining exports, construction and other parts of the economy that have been subdued, the end of the investment boom should lead to a more balanced economy reflecting less pressure on the interest rates and the A$.

For investors there are several implications including:

- Ongoing pressure for lower interest rates as the risk of an overheating economy subsides. This means that term deposit rates are likely to fall further in the years ahead.

- The best has likely been seen for the A$, implying less need to hedge global shares back to Australian dollars.

- Resources shares are currently cheap and should experience a cyclical rebound when confidence in global growth improves.

- However, beyond a short-term bounce it’s likely that the cooling of the mining boom will allow a return to a more balanced share market with domestic cyclicals likely to perform better.

This material has been provided for general information purposes and must not be construed as investment advice. This material has been prepared without taking into account the investment objectives, financial situation or particular needs of any particular person. Investors should consider obtaining professional investment advice tailored to their specific circumstances prior to making any investment decisions and should read the relevant Product Disclosure Statement.