The ALP has proposed that if it wins Government at the next election it will scrap cash refunds that are currently paid to investors with surplus imputation credits they receive from shares that they own which pay franked dividends.

Bill Shorten claims that only the wealthy will pay the tax, clearly continuing his class warfare with ‘the big end of town’.

He also said “a small number of people will no longer receive a cash refund but they will not be paying any additional tax”.

With all due respect to a potential future Prime Minister, this is rubbish!

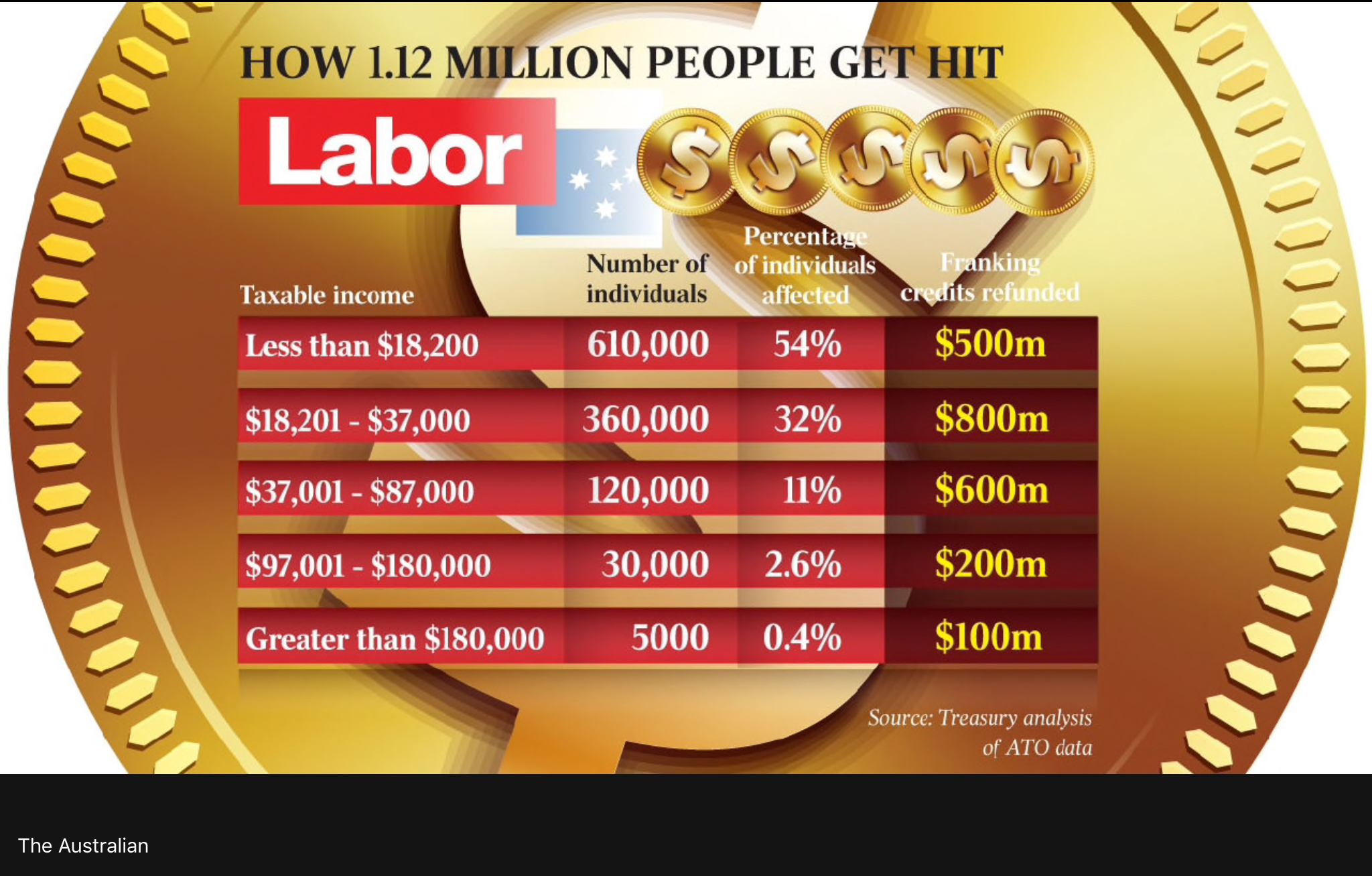

The Australian reports today that Treasury analysis of official tax data shows the largest group of people to be hit by Labor’s $59bn tax grab will be those receiving annual incomes of less than $18,200, the majority who receive the Age Pension.

In fact the likely number of people hit by this proposal is estimated at well over 1 million, bringing into question the ALP’s definition of small.

The current effective tax free threshold for a retiree couple over age 65 is around $29,000 each, courtesy of the Seniors Australian Tax Offset and of course the $18,200 tax free threshold that applies to everyone.

Therefore any retiree who’s taxable income is less than that, is currently not paying tax and at risk of having their surplus imputation credits retained by the ATO.

The whole point of dividend franking – introduced by a Labor treasurer Paul Keating of course was to stop the double taxation of dividends.

Dividends have to be paid by companies out of profits which have already paid company tax. In the old pre-Keating world those dividends would then be taxed a second time as personal income.

Under the Keating change you would get a ‘credit’ for the company tax paid on the dividend, you would then still be taxed at your full marginal tax rate on the underlying income out of which the dividend was paid.

Critically, if your marginal tax rate was lower than the 30% company tax rate, you still paid “too much” tax. That is why Peter Costello legislated the cash return of that overpayment in 2000.

If the ALP proposal becomes law, this would result in high income earners gaining the full benefit of dividend imputation but retirees and low income earners being discriminated against and unable to use the tax credits. In other words retirees would become one of the few groups in the country to pay double taxation on their dividends. The very people the ALP are alleging to protect are those most likely to lose from this proposal.

So how much do retirees (including those with Self Managed Super Funds in pension phase) stand to lose from this proposal?. The table below sets out different levels of investment in fully franked dividend paying investments and the corresponding potential loss of income for retirees.(assuming retirees are below effective tax free threshold)

|

Investment Level |

Dividend Rate (fully franked) |

Franked Income |

Imputation Credit |

Cut to Retiree income under ALP proposal |

|---|---|---|---|---|

|

$100,000 |

5% |

$5,000 |

$2,142 |

$2,142 |

|

$200,000 |

5% |

$10,000 |

$4,285 |

$4,285 |

|

$300,000 |

5% |

$15,000 |

$6,428 |

$6,428 |

|

$400,000 |

5% |

$20,000 |

$8,571 |

$8,571 |

|

$500,000 |

5% |

$25,000 |

$10,714 |

$10,714 |

|

$600,000 |

5% |

$30,000 |

$12,857 |

$12,857 |

GEM Capital is not opposed to tax reform, but we are opposed to leaders using the tax system as a political wedge for political gain that disadvantages the retiree sector.

We are deeply concerned that a potential future Government can propose in an incredibly short time frame, in a retrospective manner, such a drastic reduction for retirees’ income. Retirees have limited capacity to increase their earnings through employment which makes them a very vulnerable segment of the community to sudden changes in Government policy.

GEM Capital will be contributing to media articles in the coming weeks on this issue and will also be talking with politicians of both sides of politics with a view of broadening their perspective on the issue and at the same time represent the interests of retirees.

Feel free to share this article with anyone you believe may be impacted by this proposal.