This article appeared in the Weekend Australian Financial Review during the month of September 2018.

With the Coalition’s acts of self harm, the prospect of Bill Shorten’s imputation credit concoction becoming law, appear more likely.

Originally aimed at the “big end of town” it is important for investors to understand whether they are in fact impacted by this proposal. Since the original announcement in March by the ALP to scrap imputation credit cash refunds, a concession to pensioners, and to some SMSF’s has been announced. The concessions allow for the cash payment of surplus imputation credits to continue for those on the age pension or allowances, or for a SMSF that has a member receiving age pension, as at 28thMarch 2018.

While this concession may lead to some SMSF’s thinking about recruiting a new member who is in receipt of an age pension to the fund, I would suggest SMSF trustees first consider the potential estate planning fallout from adding new members to their fund before proceeding.

The group left most exposed to Shorten’s attack are self funded retirees and SMSF’s, particularly those in pension phase. A perverse outcome of the proposal is that high income earners and ultra wealthy Individuals are likely to be largely unaffected leaving those such as middle class retirees bearing the brunt.

High profile fund manager, Geoff Wilson believes that “Investors should not give up the fight. If Labor wins government at the next election, it may either realise the error of its ways due to public protest and abandon this flawed policy, or have it blocked in the Senate”

Therefore it would be wise to hasten slowly before making changes to investors portfolio’s in response to this proposal, however I am of the view that investors should begin thinking about how they may react if the proposal is ultimately legislated.

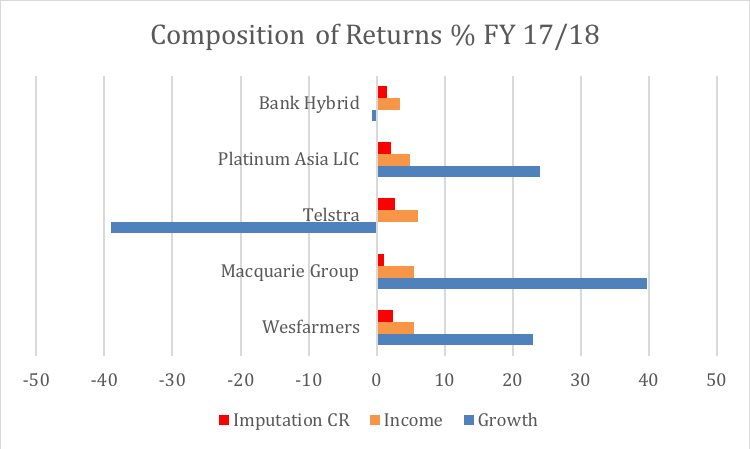

Firstly, investors need to quantify the magnitude of the potential change on an asset by asset basis. To illustrate this the graphic below shows total shareholder return of some Australian securities over the last financial year dissected between growth, income and imputation credit.

Source: IRESS

The message here is clear, total return is the main game, and investors need to keep the value of imputation credits in perspective. A focus on investment fundamentals such as company earnings, which ultimately drive value, rather than focussing simply on franking would be of far more benefit to investors.

Bank Hybrids which have become a retail investor favourite should be reviewed as a material component of the return consists of the imputation credit. Rather than focusing just on tax however, bank hybrids should be reviewed in light of the ALP’s proposed changes to negative gearing and its likely impact on the residential property market and by extension, bank earnings.

Investors in listed investment companies should not panic. In our conversations with management of listed investment companies, it is clear they are already considering their own plan B which might involve a change in legal structure to protect investors from fallout of the ALP proposal.

Those investors who use multiple investment structures, such as SMSF’s, family trusts and or companies to house their wealth, should analyse which of those structures are likely to be able to continue to use imputation credits. The aim would be to own assets paying franked income in structures where the imputation credit can be utilised, and own assets paying unfranked income in structures that can not.

Investment managers investing in global shares are one of the beneficiaries from a removal of imputation credit cash refunds. Well known names such as Magellan, Montgomery Investment Management and Platinum Asset Management are likely to attract investors into their ASX listed investment trusts that pay unfranked income alongside solid long term performance track records.

So it’s time to plan now, and act later, unless investors wish to take up Geoff Wilson’s call and participate in online petitions such as those being conducted by Wilson Asset Management and Plato Asset Management.

Here is a link to Wilson Asset Management's online petition if you have not already joined it.